Municipals were firmer Thursday following a stronger U.S. Treasury session while municipal bond mutual funds reported the second consecutive week of inflows. Equities closed the session mixed.

Triple-A yields fell one to five basis points while USTs saw gains of seven to nine basis points. The moves pushed muni to UST ratios slightly higher.

The two-year muni-to-Treasury ratio Thursday was at 66%, the three-year at 67%, the five-year at 68%, the 10-year at 67% and the 30-year at 85%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 65%, the three-year at 66%, the five-year at 66%, the 10-year at 66% and the 30-year at 82% at 3:30 p.m.

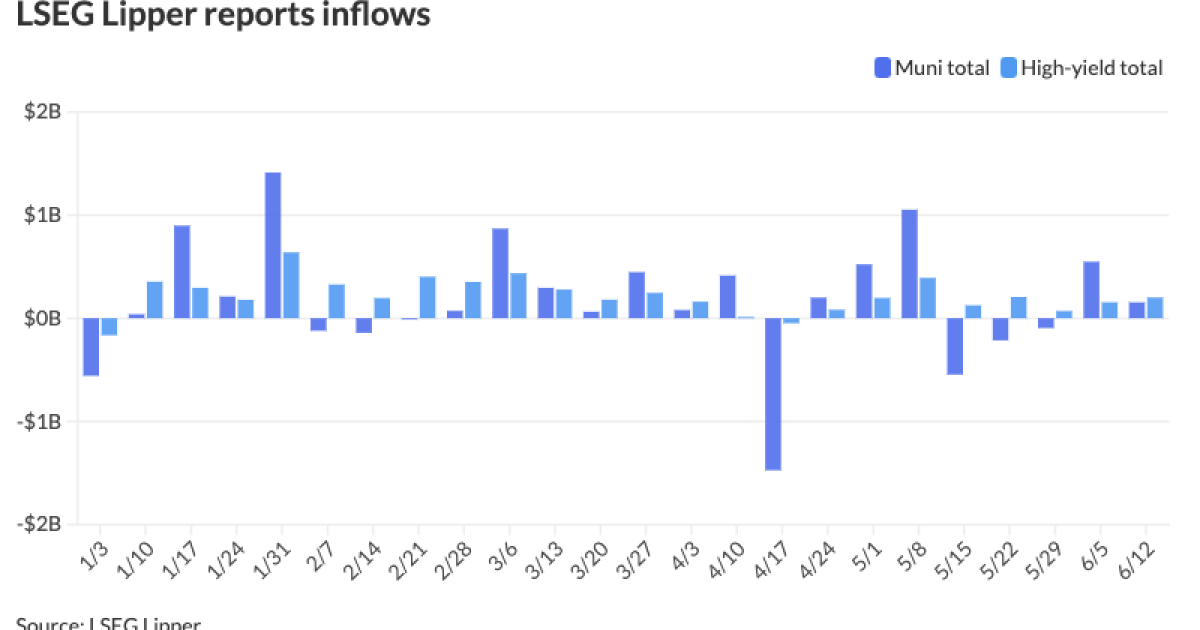

Municipal bond mutual funds saw inflows as investors added $154.2 million to the funds after $547.9 million of inflows the week prior, according to LSEG Lipper. Inflows

High-yield continued to show strength, with inflows of $201.5 million after $154.7 million of inflows the previous week.

Base rates in the muni market have been unable to keep pace with the UST market rally, said J.P. Morgan strategists, led by Peter DeGroot.

Triple-A high-grade muni yields have rallied 23 to 28 basis points month-to-date, falling behind with USTs across most of the curve, following the underperformance last month.

“Even after this week’s rally, absolute yields look attractive in the context of the trading range over the past three years, May’s underperformance versus taxable fixed-income, and our longer-term projections for lower rates this year,” J.P. Morgan strategists said.

The 10-year MMD spot has corrected by 10 basis points or more four times so far this year after a rally, said Kim Olsan, senior vice president of municipal bond trading at FHN Financial.

“The gyrations in USTs based on missed or exceeded economic data in recent months — and subsequent FOMC communications — is something that municipals are not set up to fully absorb,” she said.

The current cycle occurs at the beginning of summer seasonals when more than $100 billion — or around $33 billion between June and August — is scheduled to mature or be called, she said.

However, the monthly $33 billion figure is $7 billion less than the five-year monthly supply average figure, Olsan noted.

“What the strength post-CPI did offer was distribution of syndicate balances — bonds bought close to AAA spot levels saw interest develop that led to secondary bidsides moving tighter,” she said.

Trading in the Bergen County Improvement Authority, New Jersey, (Aaa/NR/) 5s due 2044, issued in the first week of this month at 3.68%, “found buyers about 15 basis points tighter,” Olsan said.

“Actively traded in California, Massachusetts, Washington and Connecticut GOs (and all having priced or scheduled to price during Q2) tightened up,” she said.

California GO 5s due 2034 traded at 2.88% or -4/MMD, “well through trading in the bond during May at +10/MMD,” she said.

Meanwhile, Vermont GOs sold in the competitive market on June 6 ”found buyers supporting negative spreads in the 10-year range,” Olsan said.

Overall, the curve has been shifted by price improvements once more, she noted.

Gains pushed yields between 2027 and 2037 above 3.00%, “likewise forcing buyers in search of longer-duration 3.00%-plus yields to extend toward the 15-year range,” she said.

The 2039-2044 area should “find greater demand” if levels hold in the coming week with the supply increase, according to Olsan.

“Other structures that may find support are short-call 5% coupons, trading with ample discounts to 2026-2027 options at yields over 3.50%,” she said.

In the primary market Thursday, BofA Securities priced for the Health, Education and Housing Facility Board of the County of Shelby, Tennessee (/BBB+/BBB+/) $315 million of Baptist Memorial Health Care health care revenue refunding and improvement bonds. The first tranche, $150.53 million of fixed-rate mode bonds, Series 2024A, saw 5.25s of 9/2034 at 3.67% and 5.25s of 2039 at 3.89%, callable 3/1/2034.

The second tranche, $165.17 million of term rate mode bonds, Series 2024B, saw 5s of 9/2049 with a mandatory tender date of 9/1/2029 at 3.75%, callable 6/1/2029.

In the competitive market, Denton, Texas, (/AA+/AA+/) sold $120.45 million of GO refunding and improvement bonds, with 5s of 2/2025 at 3.33%, 5s of 2029 at 2.99%, 5s of 2034 at 3.05%, 5s of 2039 at 3.39% and 4s of 2044 at 4.10%, callable 2/15/2034.

Muni CUSIP requests rise

Municipal CUSIP request volume rose in May on a year-over-year basis, following an increase in April, according to CUSIP Global Services.

For municipal bonds specifically, there was an increase of 51.5% month-over-month and an 8.4% increase year-over-year.

For the specific category of municipal bond identifier requests, there was an increase of 48.8% month-over-month and requests are up 7% on a year-over-year basis.

Texas led state-level municipal request volume with a total of 143 new CUSIP requests in May, followed by New York (102) and California (90).

AAA scales

Refinitiv MMD’s scale was bumped up to three basis points: The one-year was at 3.13% (-2) and 3.08% (-3) in two years. The five-year was at 2.89% (-1), the 10-year at 2.83% (-1) and the 30-year at 3.73% (unch) at 3 p.m.

The ICE AAA yield curve was bumped three to five basis points: 3.18% (-3) in 2025 and 3.11% (-3) in 2026. The five-year was at 2.87% (-4), the 10-year was at 2.82% (-5) and the 30-year was at 3.70% (-4) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was bumped up to two basis points: The one-year was at 3.18% (-2) in 2025 and 3.11% (-2) in 2026. The five-year was at 2.89% (-2), the 10-year was at 2.86% (-2) and the 30-year yield was at 3.73% (unch), at 4 p.m.

Bloomberg BVAL was bumped one to three basis points: 3.17% (-3) in 2025 and 3.12% (-2) in 2026. The five-year at 2.90% (-2), the 10-year at 2.83% (-2) and the 30-year at 3.72% (-2) at 3:30 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.696% (-7), the three-year was at 4.432% (-8), the five-year at 4.240% (-9), the 10-year at 4.241% (-9), the 20-year at 4.494% (-8) and the 30-year at 4.398% (-9) near the close.