Federal Reserve Chair Jerome Powell’s speech in Jackson Hole Friday removed any uncertainty of a rate cut at the Fed’s September meeting, pushing U.S. Treasury yields lower on the short end, with municipals following suit, while stocks rallied on the news.

“Powell has rung the bell for the start of the cutting cycle,” said Seema Shah, chief global strategist at Principal Asset Management. “The Federal Reserve now has strong confidence about inflation’s path forward — it is time to shift to the other side of the dual mandate, and labor market risks now have their full attention.”

When Powell referred to “humility,” it “is a direct nod to their continued data dependent approach,” she said. The August employment report will determine the magnitude of the cut, Shah added. “If the labor market shows signs of further cooling, the Fed will cut with conviction.”

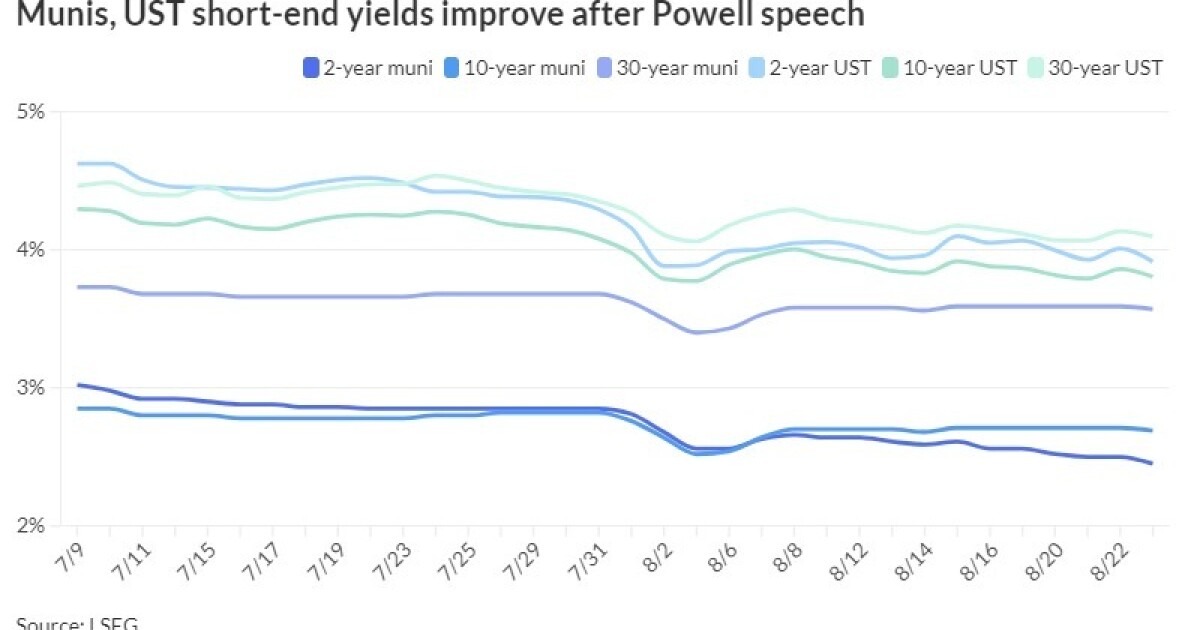

Municipal triple-A curves saw yields fall up to five basis points on the short end while Treasuries saw the two-year fall 10 basis points on the day.

Muni to UST ratios rose slightly as municipals underperformed the taxable moves.

The two-year muni-to-Treasury ratio Friday was at 63%, the three-year at 66%, the five-year at 66%, the 10-year at 71% and the 30-year at 87%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 63%, the three-year at 64%, the five-year at 65%, the 10-year at 69% and the 30-year at 87% at 4 p.m.

“At this point, it is hard to see catalysts that may reverse the ratio cheapening without a sizable Treasury market selloff,” noted BofA Global Research strategists Yingchen Li and Ian Rogow. 10- and 30-year muni ratios could possibly climb another five percentage points “based on technical readings,” if Treasuries keep rallying.

They said neither increased muni market supply, nor the Treasury market flattening rally, ”can change quickly.”

The calendar next week largely continues “the elevated pace of primary market volume seen since May, against a backdrop of broadly supportive fund flows (LSEG inflows for eight consecutive weeks), somewhat better dealer positions (although still heavy), mid-August reinvestment to spend, but lighter late summer attendance,” said J.P. Morgan strategists led by Peter DeGroot.

Municipal investors will be greeted with about $8.86 billion of supply for the final week of August, down from total sales of $9.537 billion this week.

There are 15 deals over $100 million on the negotiated calendar, led by $2.6 billion of general obligation bonds from California, nearly $1.8 billion of which is a refunding, while Chicago is slated to bring $1.003 billion of AMT and non-AMT Chicago O’Hare International Airport revenue bonds and San Antonio, Texas, is set to price Wednesday $763.795 million of electric and gas systems revenue refunding bonds.

The competitive calendar is lighter on deals over $100 million, led by gilt-edged Hamilton County, Tennessee, with $229.31 million of general obligation bonds selling on Tuesday.

“For all purposes, short of a recession or unexpected economic or market crisis, the Fed will likely not be pressured to get ahead of the [UST] curve, even after its first rate cut,” Li and Rogow said. “As such, flattening in the Treasury curve will continue to put some pressure on muni ratios.”

But muni investors ”could take some comfort that ratio cheapening usually comes with lower yields,” BofA strategists said.

“Muni hedgers, however, need to exercise some caution with hedge ratios; it requires additional caution if hedgers are shorting the back end of the Treasury curve,” they added.

J.P. Morgan strategists said as the market approaches “what promises to be an eventful fall, we brace for a volatile rates backdrop with outsized market reactions to the release of non-consensus economic data, a particularly loud election season, an expected Fed easing cycle, and including a higher and volatile municipal issuance calendar with market reception governed by the pace of fund flows and changeable nature of ETF flows in particular.”

AAA scales

Refinitiv MMD’s scale was bumped: The one-year was at 2.51% (-5) and 2.45% (-5) in two years. The five-year was at 2.42% (-4), the 10-year at 2.69% (-2) and the 30-year at 3.57% (-2) at 3 p.m.

The ICE AAA yield curve was better across the curve: 2.60% (-1) in 2025 and 2.51% (-2) in 2026. The five-year was at 2.43% (-3), the 10-year was at 2.66% (-4) and the 30-year was at 3.58% (-3) near the close.

The S&P Global Market Intelligence municipal curve was bumped: The one-year was at 2.57% (-5) in 2025 and 2.51% (-5) in 2026. The five-year was at 2.42% (-5), the 10-year was at 2.66% (-2) and the 30-year yield was at 3.54% (-2) at 3 p.m.

Bloomberg BVAL was better: 2.52% (-5) in 2025 and 2.48% in 2026 (-5). The five-year at 2.47% (-5), the 10-year at 2.67% (unch) and the 30-year at 3.58% (unch) at 4 p.m.

Treasuries were firmer.

The two-year UST was yielding 3.913% (-10), the three-year was at 3.727% (-9), the five-year at 3.65% (-8), the 10-year at 3.805% (-6), the 20-year at 4.188% (-4) and the 30-year at 4.096% (-4) at the close.

Powell’s speech clear

The markets took Powell’s

While offering no specifics, he said, “The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

Upside inflation risks dropped. Powell said, “my confidence has grown that inflation is on a sustainable path back to 2%.”

Vowing to meet the dual mandate, he added, “With an appropriate dialing back of policy restraint, there is good reason to think that the economy will get back to 2% inflation while maintaining a strong labor market. The current level of our policy rate gives us ample room to respond to any risks we may face, including the risk of unwelcome further weakening in labor market conditions.”

ING Chief International Economist James Knightley agreed. “If we get a sub 100k on payrolls and the unemployment rate ticking up to 4.4% or even 4.5% then 50bp looks more likely,” he said. “If payrolls come in around the 150k mark and unemployment rate stays at 4.3% or dips to 4.2% we can safely say it will be a 25bp.”

Noting criticism for “potentially waiting too long to raise rates,” DWS U.S. Economist Christian Scherrmann said, “Powell indicated that they have learned their lessons — perhaps a soft hint that the Fed is ready to cut rates by more than 25 basis points if economic conditions warrant.”

While he said he doesn’t believe a half-point cut is needed now, “it certainly gives the markets a bit of what they have been asking for.”

Mortgage Bankers Association SVP and Chief Economist Mike Fratantoni said the September cut “will be the first in a series that should bring the federal funds target down significantly over the next 18 months.”

Labor market weakening indicates to the Fed there won’t be a reacceleration of inflation, he said. “There is certainly a risk that the unemployment rate could rise faster and further than the Fed would like, but Chair Powell indicated that they are watching and would react to such a further softening in the job market.”

“Powell sounded quite relieved to be able to effectively pre-announce a cut, after what has clearly been a much longer battle to get inflation down than the Fed and most others expected,” said Fitch Ratings Chief Economist Brian Coulton.

The Fed doesn’t appear seriously concerned “about the risk of an imminent recession and a wave of job losses,” but sees the labor market cooling as lowering the risk of elevated wage growth, which would stoke inflation, he said.

“This is helping provide confidence that recent progress on disinflation will be sustained and that some easing in restrictiveness is warranted,” Coulton said, “but the policy easing path post September will be a gradual one.”

Dan Siluk, head of global short duration and liquidity at Janus Henderson Investors, said, “The speech was cautiously optimistic, suggesting that inflation is on a sustainable path back to the target without necessitating a sharp increase in unemployment. This may reassure investors about the potential for a soft landing.”

Equities and credit markets firmed after the speech, he noted. Hedging on the magnitude of the September cut, “rate markets have not decisively moved to firmly price in either a 25 basis point or a 50 basis point adjustment for September, remaining somewhere in the middle of that range.”

Primary to come:

California (Aa2/AA-/AA/) is set to price $2.606 billion of general obligation bonds Tuesday, consisting of $810.875 million of new-money, serials 2026-2029, 2031, 2033, 2036, 2044, terms 2049, 2054; and $1.795 billion of refunding GOs, serials 2025-2037, 2039, 2044. BofA Securities.

Chicago (//A+/) is set to price $1.003 billion of AMT and non-AMT Chicago O’Hare International Airport General Airport Senior Lien Revenue Bonds, consisting of $563.945 million of AMT bonds, serials 2036-2044, terms 2048, 2053, 2059; and $440.045 million of non-AMT bonds, serials 2036-2044, terms 2048, 2053, 2059. Wells Fargo Bank, N.A. Municipal Finance Group.

San Antonio, Texas, (Aa2/AA-/AA-/) is set to price Wednesday $763.795 million of electric and gas systems revenue refunding bonds, consisting of $489.525 million of Series 2024D and $274.27 million of Series 2024E. J.P. Morgan Securities LLC

The Utah Transit Authority is set to price Wednesday $469.915 million in tow series, $327.39 million of sales tax revenue refunding bonds, Series 2024, (Aa2/AA+/AA/), serials 2030-2040; and $94.525 million of subordinated sales tax revenue refunding bonds, Series 2024, (Aa3/AA/AA/), serials 2037-2040. Wells Fargo Bank, N.A. Municipal Finance Group.

The Allegheny County Sanitary Authority (Aa3/AA-//) is on the day-to-day calendar with $361.595 million of sewer revenue refunding bonds, serials 2024-2044, terms 2049, 2055. PNC Capital Markets LLC.

The Illinois Finance Authority (Aa3/AA-//) is on the day-to-day calendar with $281.02 million of Endeavor Health Credit Group revenue refunding bonds, serials 2030-2034. BofA Securities.

The Cabarrus County Development Corp., North Carolina, (Aa1/AA+/AA+/) is on the day-to-day calendar with $204.63 million of limited obligation refunding bonds, serials 2025-2044. BofA Securities.

The Maine Health and Higher Educational Facilities Authority (A1///) is set to price Tuesday $189.28 million of Northeastern University revenue bonds. Morgan Stanley & Co. LLC.

Pennsylvania State University (Aa1/AA//) is set to price Tuesday $157.345 million of Series 2024 bonds. Morgan Stanley & Co. LLC.

The Texas Veterans Land Board (Aaa///) is set to price Wednesday $135 million of taxable refunding veterans bonds, term 2051. Jefferies LLC.

The Indiana Finance Authority (A3/A-//) is set to price Wednesday $133.96 million of Hendricks Regional Health health facility revenue refunding bonds. Piper Sandler & Co.

Greenville, Texas, (/A//) is set to price Tuesday $128.245 million of electric system revenue and refunding bonds, serials 2027-2044, terms 2049, 2054. Jefferies LLC.

The Alaska Housing Finance Corp. (Aa2/AA+//) is set to price $127.65 million of State Capital Project Bonds II, 2024 Series A, refunding, serials 2027-2037, terms 2038, 2039. Raymond James & Associates, Inc.

The Rhode Island Commerce Corp. (A2/AA-//) is set to price Tuesday $126.485 million of Rhode Island DOT grant anticipation bonds, serials 2032-2039. BofA Securities.

The University of Kentucky (Aa3/AA//) is set to price Wednesday $101.255 million of lease purchase obligations, UK Healthcare Cancer Center Parkin project, serials 2025-2044, terms 2049, 2054. BofA Securities.

Competitive:

Hamilton County, Tennessee, (Aaa/AAA/AAA/) is set to sell $229.31 million of general obligation bonds at 10 a.m. eastern Tuesday. The issuer will also sell $22.71 million of GO refunding bonds at 10 a.m. eastern Tuesday.

Davis School District Board of Education, Utah, (Aaa///) is set to sell $100 million of GOs at 11:30 a.m. eastern Tuesday.

North Hempstead, New York, is set to sell $100.858 million of general obligation bond anticipation notes at 10:30 a.m. eastern Thursday.