Municipals were mixed in secondary trading Wednesday as the primary market took focus, led by a $1.2 billion deal in three series from the Dormitory Authority of the State of New York. U.S. Treasury yields fell slightly and equities ended up.

Thursday’s consumer price index report is the “event of the week,” said Cooper Howard, a fixed-income strategist at Charles Schwab.

“We expect inflation to cool over time giving the Fed cover to cut rates,” he said.

The market is pricing in two rate cuts this year, and if CPI “comes in cooler than expected, it will likely cement those expectations, barring a major surprise later this year,” he said.

Municipal seasonality “plays a large role in yield direction, offering more optimal entry points at certain points in the year and conversely tighter-bid conditions when demand runs high,” said Kim Olsan, senior vice president of municipal bond trading at FHN Financial.

Current fundamentals include another month with large redemptions, with about $34 billion in called or matured bonds this month, she said.

Large-scale issuers, including state-level transportation authorities, counties and sales tax entities, have “planned volume to coincide with implied demand,” she said.

With a $9-plus billion new-issue calendar this week, issuance was heavy Wednesday.

In the competitive market the Dormitory Authority of the State of New York (Aa1///AAA/) sold $411.38 million of state sales tax revenue bonds, Series 2024A, Bidding Group 1, to Morgan Stanley, with 5s of 2026 at 3.04%, 5s of 2029 at 2.92%, 5s of 2034 at 2.98%, 5s of 2039 at 3.23% and 5s of 2041 at 3.43%.

The authority also sold $418.55 million of state sales tax revenue bonds, Series 2024A, Bidding Group 2, to J.P. Morgan. Pricing details were not available as of 3:30 p.m.

Additionally, the authority sold $397.99 million of state sales tax revenue bonds, Series 2024A, Bidding Group 3, to BofA Securities, with 5s of 3/2051 at 4.00%, 5s of 2054 at 4.06% and 5s of 2056 at 4.10%, callable 9/15/2034.

In the negotiated market, Morgan Stanley priced for Harris County, Texas, (Aaa//AAA/) $746.345 million. The first tranche, $102.03 million of permanent improvement refunding bonds, Series 2024A, saw 5s of 9/2027 at 3.01%, 5s of 2029 at 3.02%, 5s of 2034 at 3.12%, 5s of 2039 at 3.37%, 4s of 2044 at 4.15%, 5s of 2049 at 4.00% and 5s of 2054 at 4.13%, callable 9/15/2034.

The second tranche, $221.835 million of unlimited tax road refunding bonds, Series 2024A, saw 5s of 9/2025 at 3.10%, 5s of 2029 at 3.02%, 5s of 2034 at 3.12%, 5s of 2039 at 3.37%, 4s of 2044 at 4.15%, 5s of 2049 at 4.00% and 5s of 2054 at 4.13%, callable 9/15/2034.

The third tranche, $422.48 million of permanent improvement tax and revenue certificates of obligations, Series 2024, with 5s of 9/2026 at 3.06%, 5s of 2029 at 3.02%, 5s of 2034 at 3.12%, 5s of 2039 at 3.37%, 4s of 2044 at 4.15%, 5s of 2049 at 4.00% and 5s of 2054 at 4.13%, callable 9/15/2034.

Morgan Stanley priced for the District of Columbia Water and Sewer Authority (Aa2/AA+/AA/) an upsized $506.36 million of public utility subordinate lien revenue refunding bonds, Series 2024A, with 5s of 10/2025 at 3.08%, 5s of 2029 at 2.92%, 5s of 2034 at 3.02%, 5s of 2039 at 3.29% and 5s of 2044 at 3.63%, callable 10/1/2034.

J.P. Morgan priced for The University of Wisconsin Hospitals and Clinics Authority (Aa3/AA-//) $296.7 million of sustainability revenue bonds. The first tranche, $186.66 million of fixed-rate bonds, Series 2024A, saw 5s of 4/2025 at 3.30%, 5s of 2029 at 3.16%, 5s of 2034 at 3.25%, 5s of 2039 at 3.53%, 4s of 2044 at 4.17%, 5s of 2049 at 4.09% and 4.25s of 2054 at 4.38%, callable 10/1/2034.

The second tranche, $110.04 million of long-term rate bonds, Series 2024B, saw 5s of 4/2054 with a mandatory put date of 10/1/2031 at 3.35%, callable 10/1/2030.

J.P. Morgan priced for the San Diego Public Facilities Finance Authority (/AA-/AA/) $213.24 million of lease revenue and lease revenue refunding bonds, Series 2024A, with 5s of 10/2024 at 3.25%, 5s of 2029 at 2.88%, 5s of 2034 at 2.97%, 5s of 2039 at 3.23%, 5s of 2044 at 3.58%, 5s of 2049 at 3.82% and 5s of 2054 at 3.90%, callable 10/15/2034.

BofA Securities priced for the San Diego Unified School District $200 million of tax and revenue anticipation notes, Series A, with 5s of 6/2025 at 3.14%, noncall.

Wells Fargo priced for the Development Authority of Fulton County, Georgia, (Aa3/AA-//) $102.32 million of Georgia Tech Curran Street Residence Hall Project facilities revenue bonds, Series 2024, with 5s of 6/2027 at 2.95%, 5s of 2029 at 2.97%, 5s of 2034 at 3.02%, 5s of 2039 at 3.28%, 5s of 2044 at 3.76%, 5s of 2050 at 4.03%, 5s of 2056 at 4.14% and 5.25s of 2056 at 4.09%, callable 6/15/2034.

J.P. Morgan priced for the Delaware State Housing Authority (Aa1///) $100 million of non-AMT senior single-family mortgage revenue bonds, 2024 Series C, with all bonds priced at par — 3.2s of 7/2025, 3.45s of 1/2029, 3.5s of 7/2029, 3.9s of 1/2034, 3.9s of 7/2034, 4.1s of 7/2039, 4.45s of 7/2044, 4.6s of 7/2049 and 4.7s of 7/2054 — except for 6s of 1/2055 at 4.03%, callable 7/1/2033.

Overall, “the path of municipal issuance reflects the market’s impact on major funding categories for states and local municipalities,” Olsan said.

Over the past 20 years, issuance has averaged $397 billion, reaching a high in 2020 at $448 billion, she said.

This year’s “issuance rate is on pace to potentially exceed the prior high value, as deferred projects and run off of pandemic-related relief funds occurs,” Olsan said, adding a “supportive factor is that issuers are presented with competitive financing levels.”

Elsewhere, “cross-market ratios have fallen in recent years and set up a new paradigm of what is considered value,” she said.

Several periods have seen 10- and 30-year muni-UST ratios top 100%, “where 80% has long been considered the minimum standard for intermediate bonds and 90% the benchmark for long-dated munis,” according to Olsan.

“During cycles of market stress (2009, briefly in 2020), 10-year AAA yields did throw off ratios near or above 90%, however that range has moderated in recent years to settle around 70%,” she said.

The two-year muni-to-Treasury ratio Wednesday was at 64%, the three-year at 66%, the five-year at 67%, the 10-year at 67% and the 30-year at 83%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 65%, the three-year at 66%, the five-year at 67%, the 10-year at 67% and the 30-year at 82% at 3:30 p.m.

Investors, at the end of the curve, have “adjusted to 80%-range ratios with the offset of higher absolute yields,” she said.

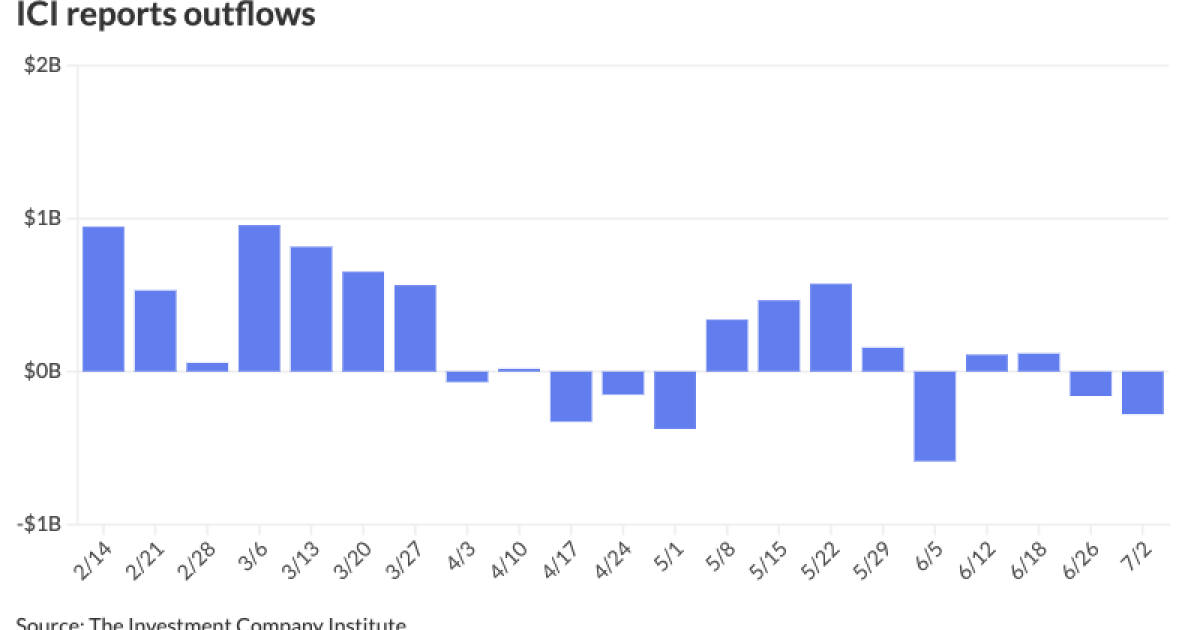

The Investment Company Institute reported Wednesday $279 million of outflows from municipal bond mutual funds for the week ending July 2 following $160 million of outflows the week prior.

Exchange-traded funds saw outflows at $391 million, following outflows of $341 million the week prior.

AAA scales

Refinitiv MMD’s scale saw bumps in one- and two-years: The one-year was at 3.00% (-4) and 2.98% (-4) in two years. The five-year was at 2.86% (unch), the 10-year at 2.85% (unch) and the 30-year at 3.73% (unch) at 3 p.m.

The ICE AAA yield curve was bumped one basis point: 3.08% (-1) in 2025 and 3.02% (-1) in 2026. The five-year was at 2.86% (-1), the 10-year was at 2.85% (-1) and the 30-year was at 3.68% (-1) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was bumped up to six basis points: The one-year was at 3.05% (-6) in 2025 and 3.01% (-5) in 2026. The five-year was at 2.86% (-2), the 10-year was at 2.85% (-1) and the 30-year yield was at 3.70% (unch) at 3 p.m.

Bloomberg BVAL was mixed: 3.09% (-4) in 2025 and 3.02% (-6) in 2026. The five-year at 2.89% (-2), the 10-year at 2.86% (+4) and the 30-year at 3.73% (unch) at 3:30 p.m.

Treasuries were slightly firmer.

The two-year UST was yielding 4.621% (flat), the three-year was at 4.388% (-2), the five-year at 4.237% (-1), the 10-year at 4.279% (-2), the 20-year at 4.576% (-2) and the 30-year at 4.471% (-2) at 4 p.m.

Primary to come

Houston is set to price Thursday a

The Cabarrus County Development Corp., North Carolina, (Aa1/AA+/AA+/) is set to price Thursday $204.63 million of limited obligation refunding bonds, Series 2024A, serials 2025-2044. BofA Securities.

Competitive

Colorado is set to price $500 million of education loan program tax and revenue anticipation notes at 11 a.m. Thursday.